Q3 2025 Crypto Analytics: Key Assets and Performance by Sectors

Bitcoin And Wide Market

Source: tradingview.com

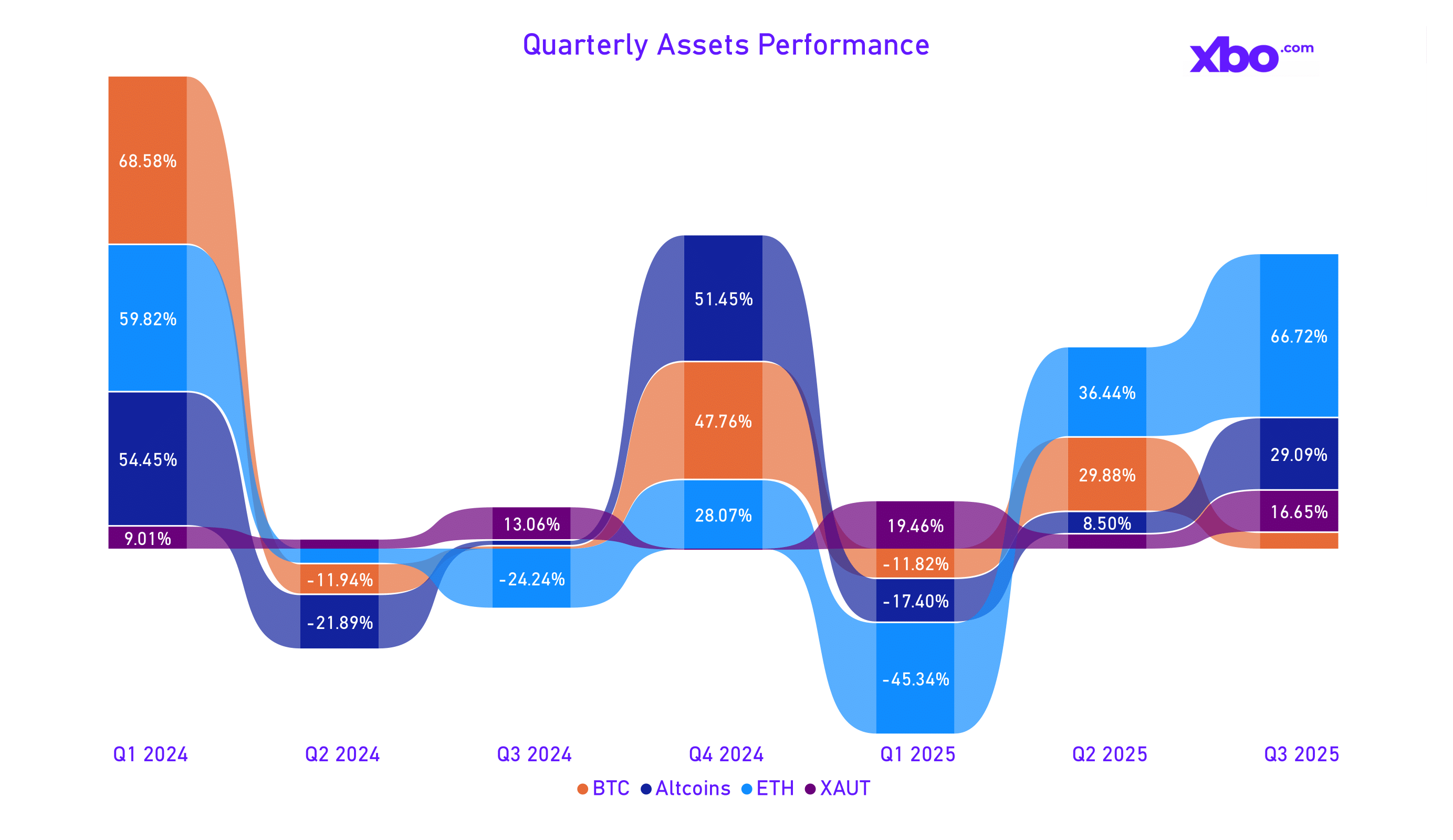

In the third quarter of 2025, Ethereum demonstrated outstanding performance, nearly doubling its growth rate compared to the second quarter. Altcoins ranked second with a total capitalization increase of 29.9%. At the same time, Bitcoin lagged, showing a gain of only 6% and falling behind spot tokenized gold, which grew by 16%. Such a gap reflects a redistribution of capital toward assets alternative to Bitcoin.

Source: tradingview.com, www.nasdaq.com, www.investing.com

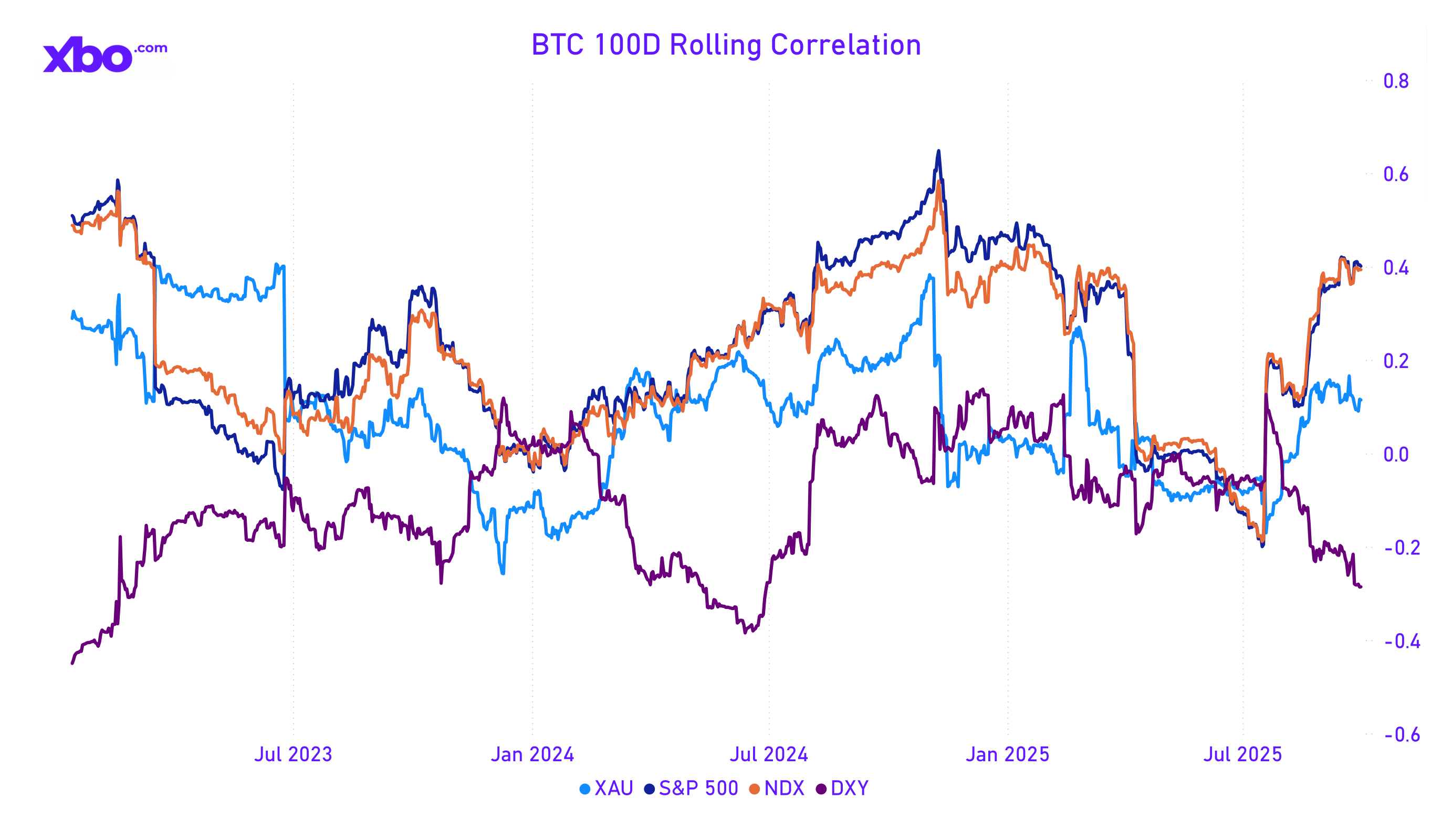

Since the start of the quarter, BTC has shown an increase in correlation with S&P 500 and Nasdaq-100 (NDX) stock indices, as well as with gold, though the connection with the latter developed more slowly. The correlation with the dollar index (DXY) decreased – a trend that traditionally accompanies BTC growth. However, the current high dependence on the stock market is perceived as a potential threat. Some analysts note the overvaluation of stock indices and warn that, if the Fed does not cut rates due to weak U.S. macroeconomic data, a correction of both the stock market and BTC is possible. In current conditions, a stronger correlation with gold would be preferable, as it could mitigate risks.

Source: bgeometrics.com

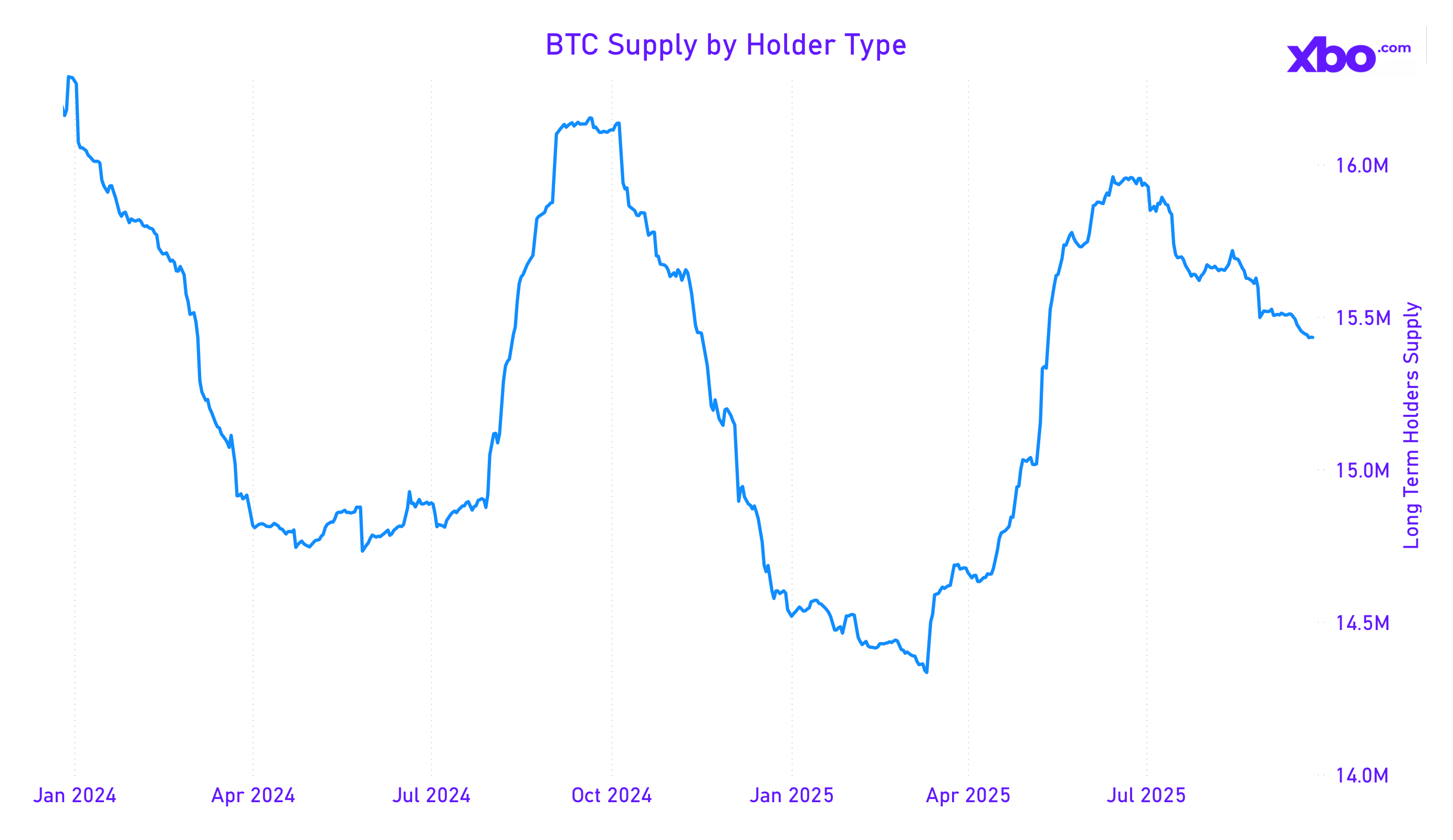

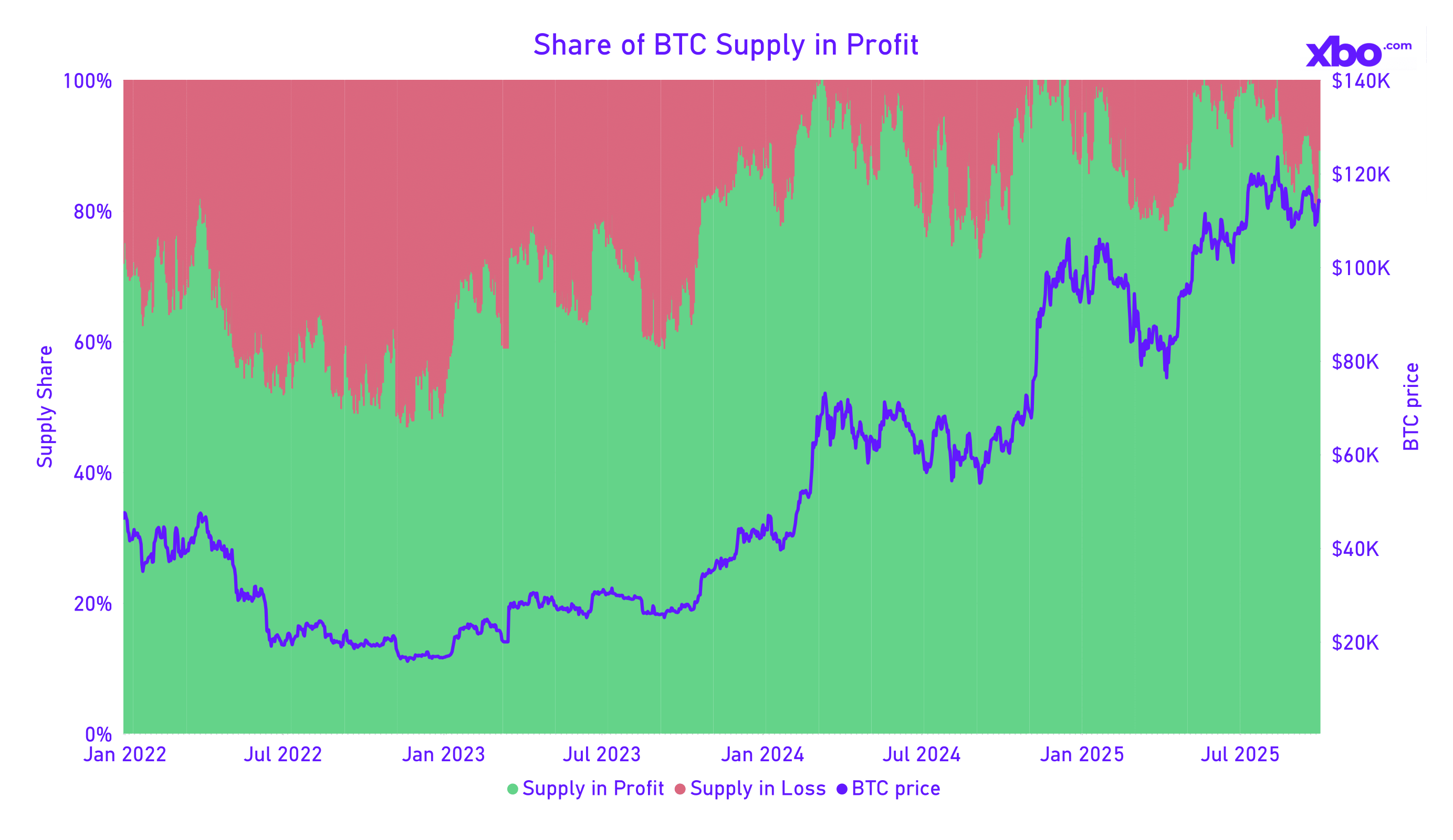

Moreover, since the start of Q3, long-term BTC holders have been actively reducing their supply, which historically signals the end of a cycle. However, the pace of current sell-offs is lower than in previous cycles, indicating caution and uncertainty among investors.

Source: cryptoquant.com

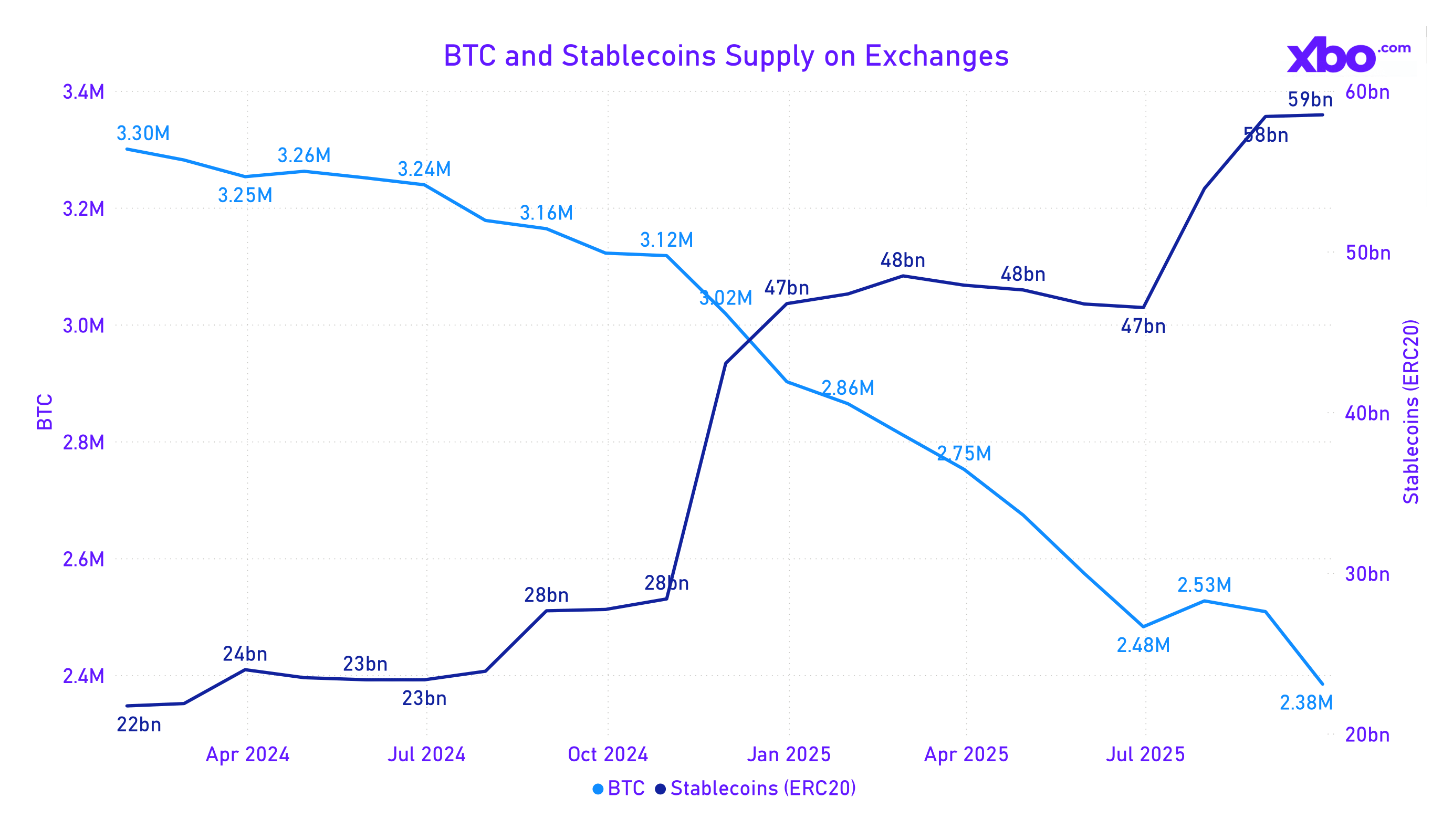

Meanwhile, exchange activity shows the opposite trend: the supply of BTC on exchanges continues to decrease, largely due to corporate treasuries increasing their reserves by 10%. Presumably, a significant portion of the withdrawn funds is linked to retail purchases. At the same time, liquidity on exchanges is growing, creating a potential "supply shock." However, not all inflows of stablecoins are directed toward buying BTC; in Q3, altcoins likely enjoyed greater demand, as evidenced by their price growth.

Source: www.theblock.co

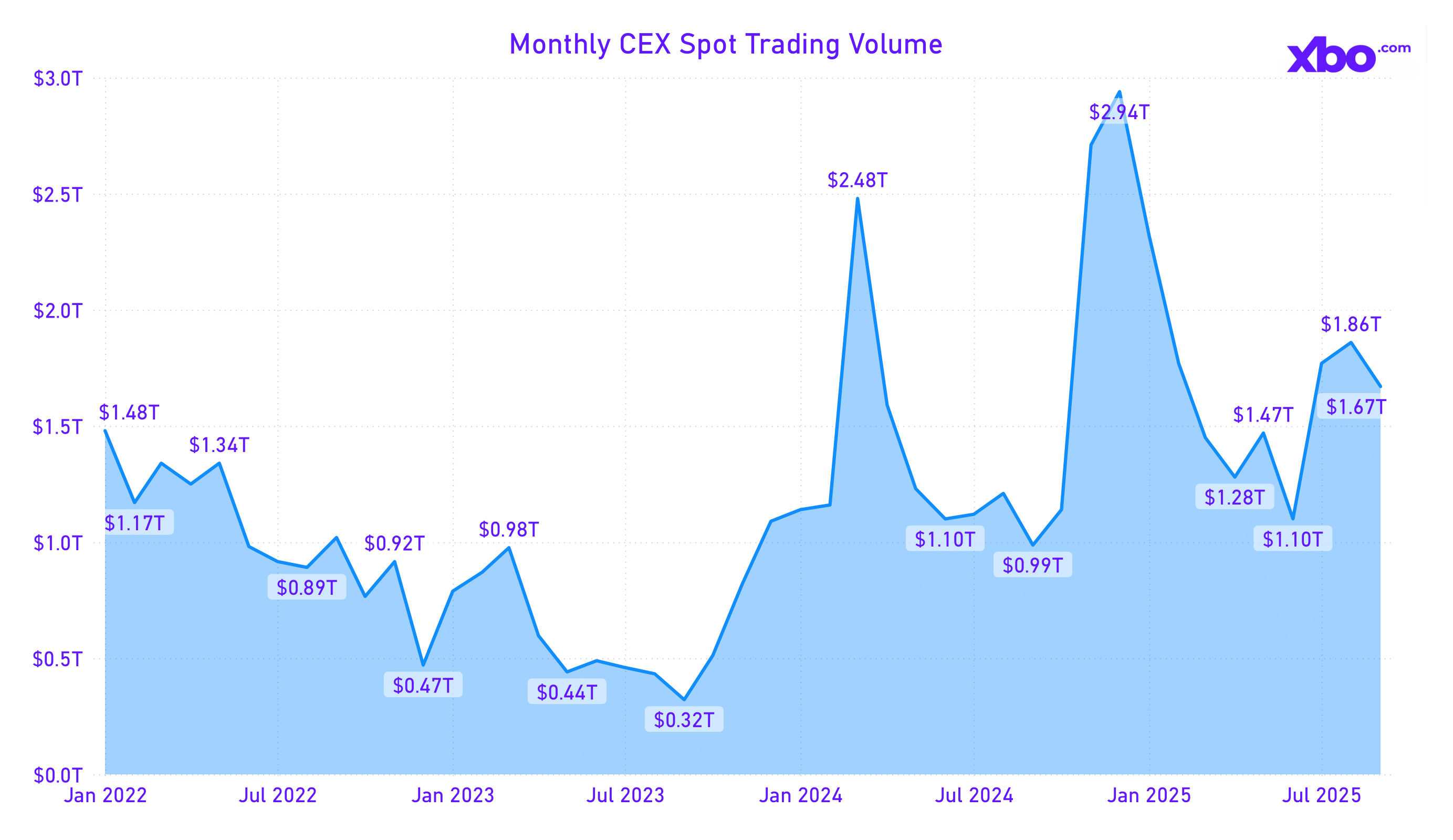

We could also observe an increase in exchange activity in the form of a cumulative rise in trading volume for the third quarter of 2025. The total amount of traded funds reached $5.3 trillion.

Source: bgeometrics.com

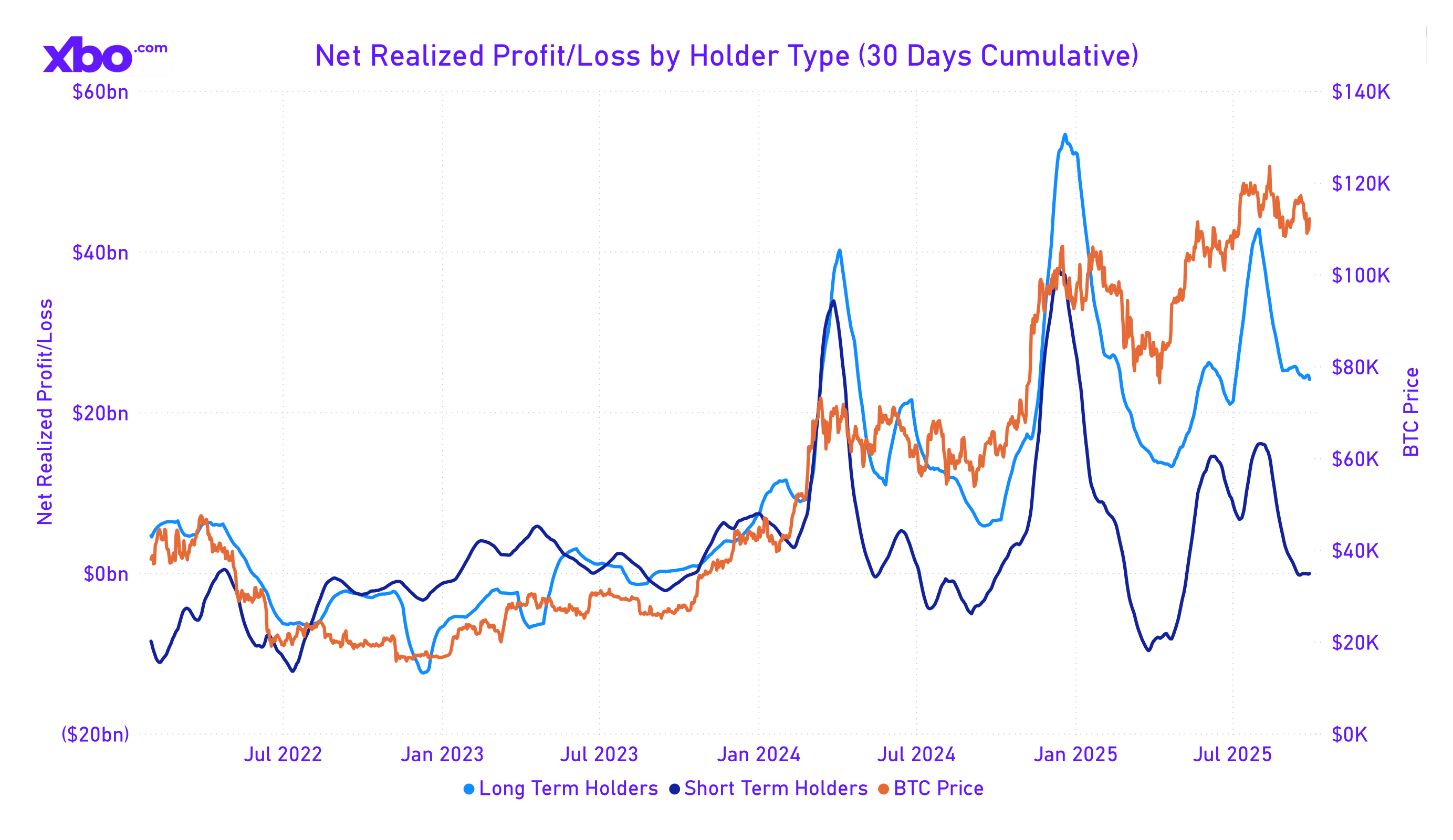

However, the sentiment of retail investors remains a key risk. By the end of Q3, short-term holders’ profit dropped to zero. Historically, this precedes a prolonged flat or deep correction, as seen at the beginning of 2025, when the correction was 30% from the ATH and lasted until April. The profit of long-term holders over the last 30 days amounted to $24 billion, despite the decline.

Source: bgeometrics.com

Although supply from long-term holders has been reduced, the market shows growth in exchange activity and liquidity, creating favorable conditions for Bitcoin. The elevated trading volume of $5.3 trillion and optimism tied to corporate treasuries point to potential for further BTC growth, possibly bypassing the expected correction. Even though risks, including high correlation with the stock market and uncertainty with macroeconomic factors such as the Fed rate, persist, the current dynamics of liquidity and demand allow for optimism in the coming months, especially with the support of the seasonal "Uptober."

Ethereum

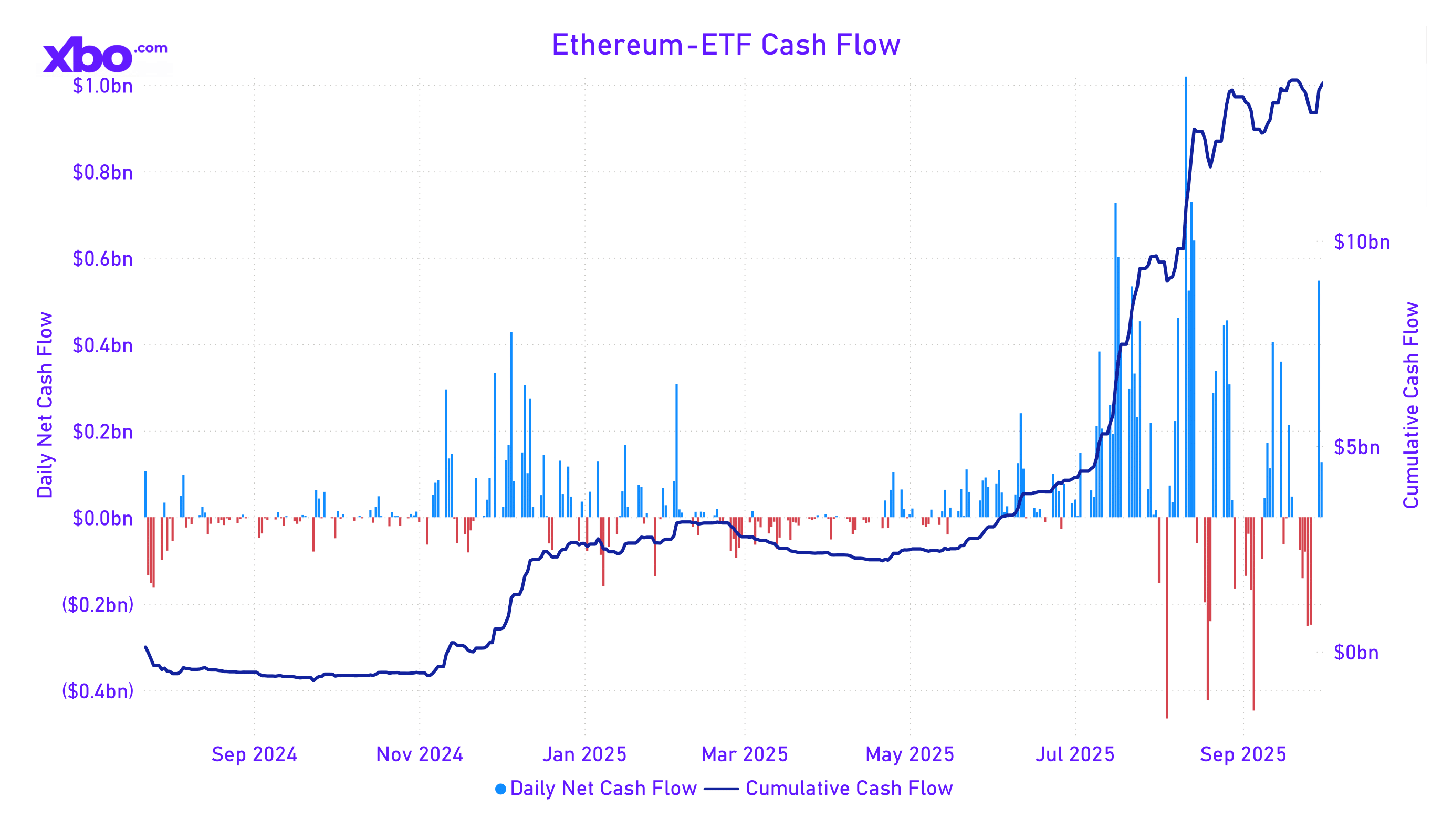

Source: farside.co.uk

In the third quarter of 2025, Ethereum (ETH) demonstrated significant price growth, achieving a 66% increase. The primary driver was an unprecedented surge in inflows to Ethereum ETFs, totaling $9.5 billion, compared to $1.7 billion in the second quarter. This growth is supported by institutional interest, including active participation from ETH treasuries of major corporations, which increased their reserves by 15%.

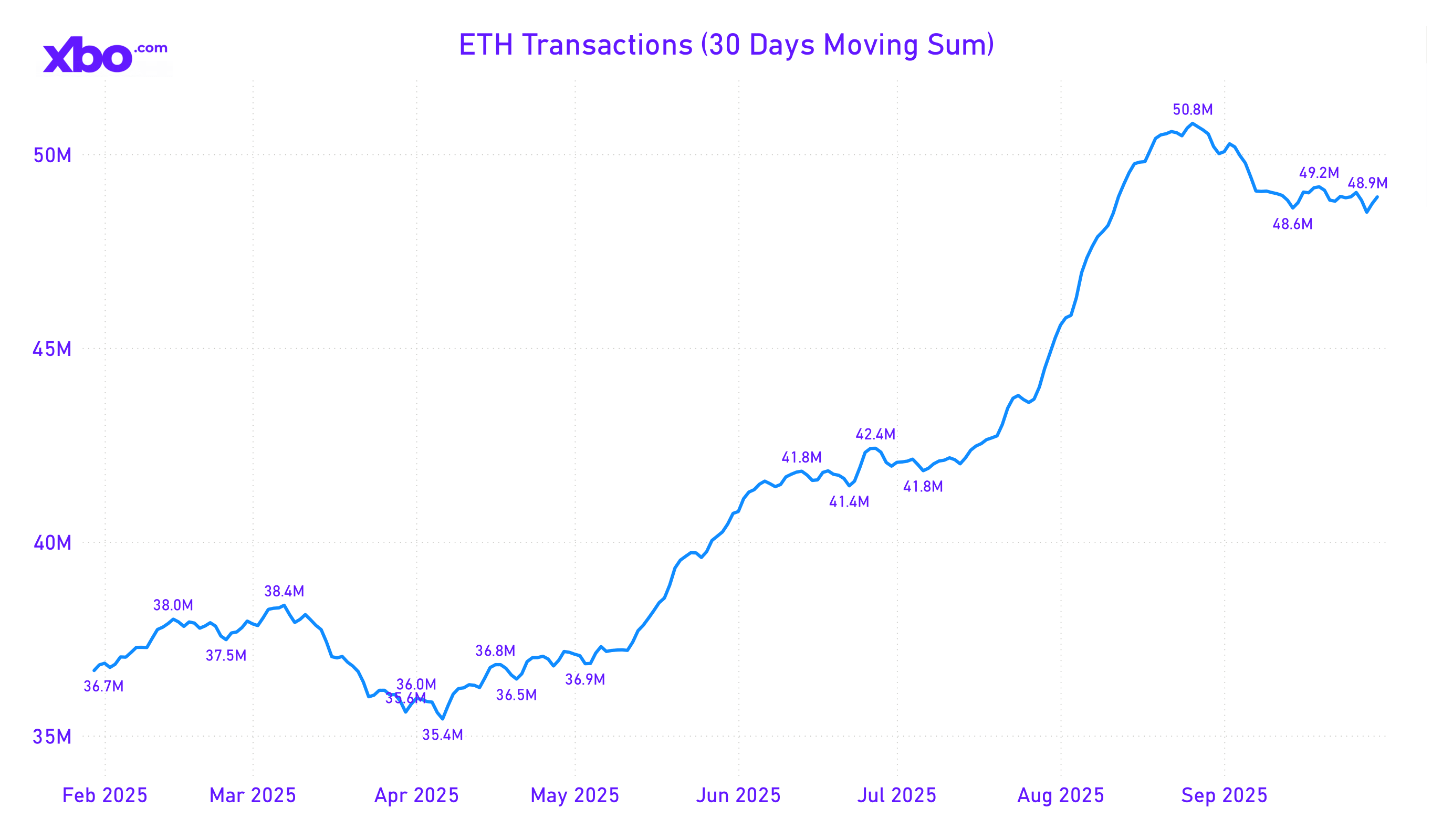

Source: app.artemisanalytics.com

A significant contribution came from the technological upgrade known as Pectra, implemented in May–June 2025. This update, which includes EIP-4844 and scalability optimizations, reduced fees by 30–40%, stimulating transaction growth. The strategy of burning ETH through increased activity paid off, particularly due to the surge in stablecoin adoption (USDC, USDT), whose turnover on the Ethereum network rose by 18%. As a result, ETH issuance once again became deflationary, with a net burn of 14,000 ETH over the quarter strengthening price dynamics.

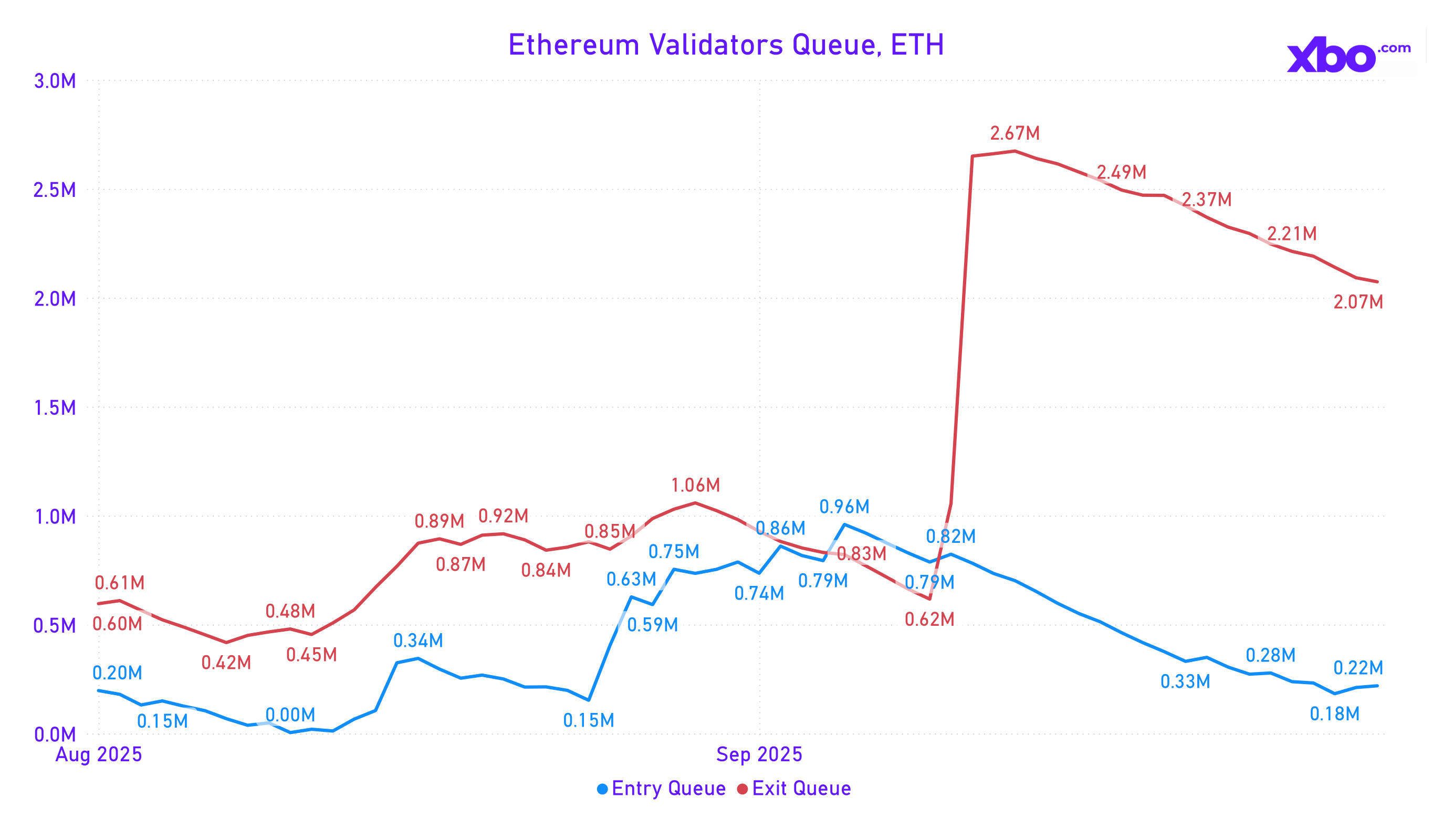

Source: www.validatorqueue.com

However, the ETH market faced a new challenge: the second-largest outflow from staking in history, exceeding 2 million ETH, with withdrawals expected in mid-to-late October 2025. This could put pressure on price growth, though analysts suggest that a significant portion will be redirected to liquid staking protocols, maintaining a balance between sellers and buyers.

Based on the above, it can be concluded that Ethereum is increasingly successful in normalizing blockchain efficiency, as it remains a key blockchain for stablecoins and RWA tokenization. According to analysts, 70% of transactions on the network are related to DeFi and stablecoins, confirming the effectiveness of the strategy to boost transactional activity. Presently, the main risks remain the reliability of ETH treasuries and the fate of the staked supply being withdrawn. It’s highly likely that it will be reinvested in liquid protocols, minimizing the impact of sell-offs.

Stablecoins and Liquidity

In 2025, a key federal regulatory step was taken – the adoption of the GENIUS Act. The bill, initiated by Senators Hagerty, Scott, Lummis, and Gillibrand on February 4, passed the Senate Banking Committee on March 13, with further approval by the Senate on June 17 and by the House of Representatives on July 17. President Trump signed it into law on July 18. The companion STABLE Act, introduced on March 26 and approved by the Committee on April 4, was integrated into the final text, forming a unified regulatory framework.

The GENIUS Act establishes the first federal framework for stablecoins, defining them as digital assets used for payments and settlements, pegged to the U.S. dollar, excluding their classification as securities or commodities. Issuance is allowed only by permitted entities: banks and credit unions under the supervision of the Fed and OCC, as well as non-bank companies holding an OCC license, limited to $10 billion under state jurisdiction, with a prohibition on operating without a license. Reserves must comply with a 1:1 backing standard in highly liquid assets, with monthly reporting and annual audits required for issuers with a capitalization exceeding $50 billion. Oversight is conducted at both federal and state levels, with mandatory AML and BSA programs under FinCEN control. The law includes protective measures: asset redemption within two days, a ban on misleading advertising and on interest payments to holders, and a two-year moratorium on developing algorithmic stablecoins until July 2027 for risk assessment studies.

A significant increase in liquidity is expected due to mandatory 1:1 reserves in Treasuries and cash, boosting institutional and investor confidence. A 20% rise in TVL is projected for 2025, with stablecoins being integrated into banking systems to optimize payments. According to Chainalysis estimates, turnover could grow by 20–50%, with cross-border operations increasing by 16%, potentially reaching $2 trillion by 2028 thanks to regulatory clarity.

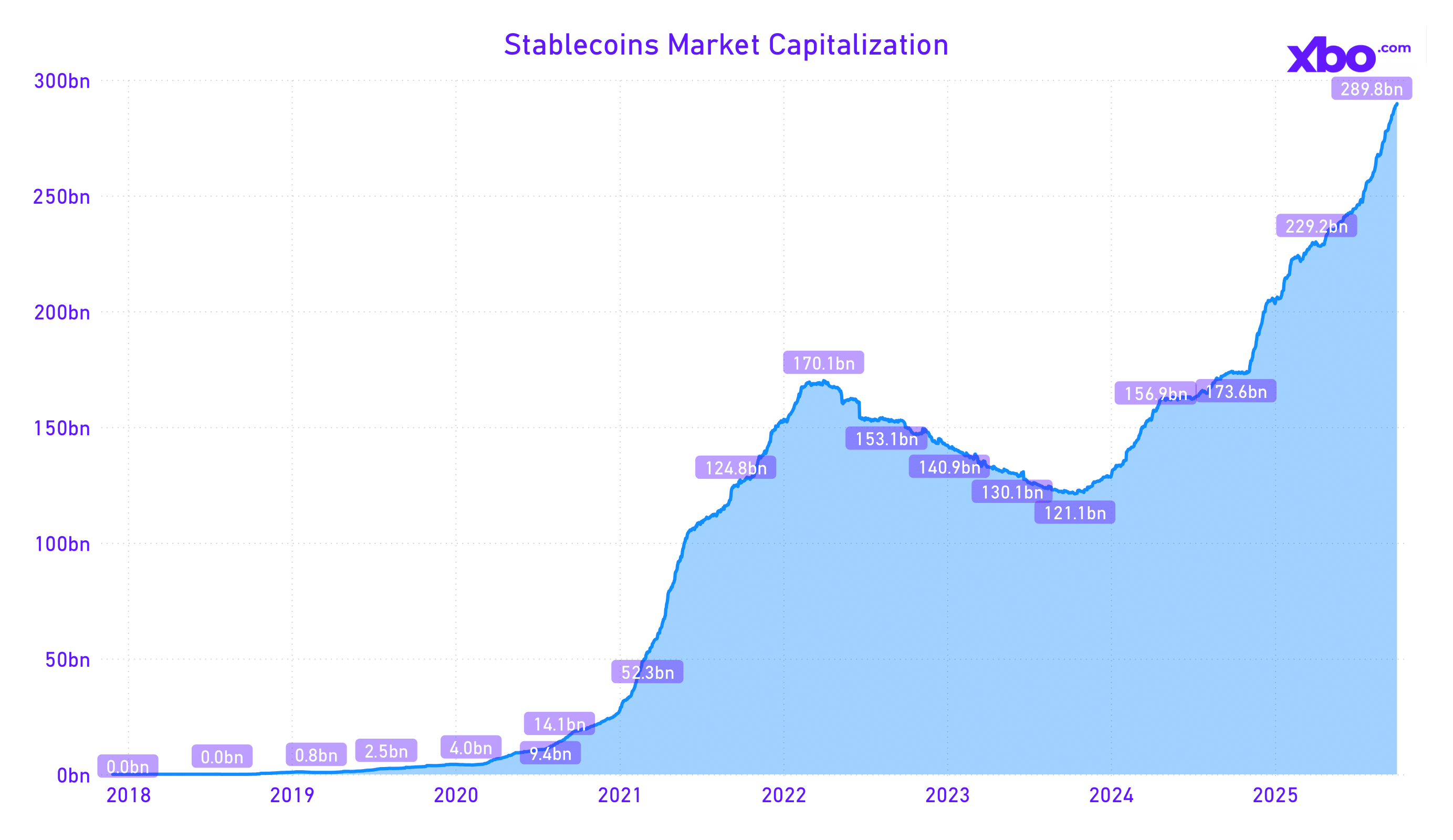

Source: app.rwa.xyz

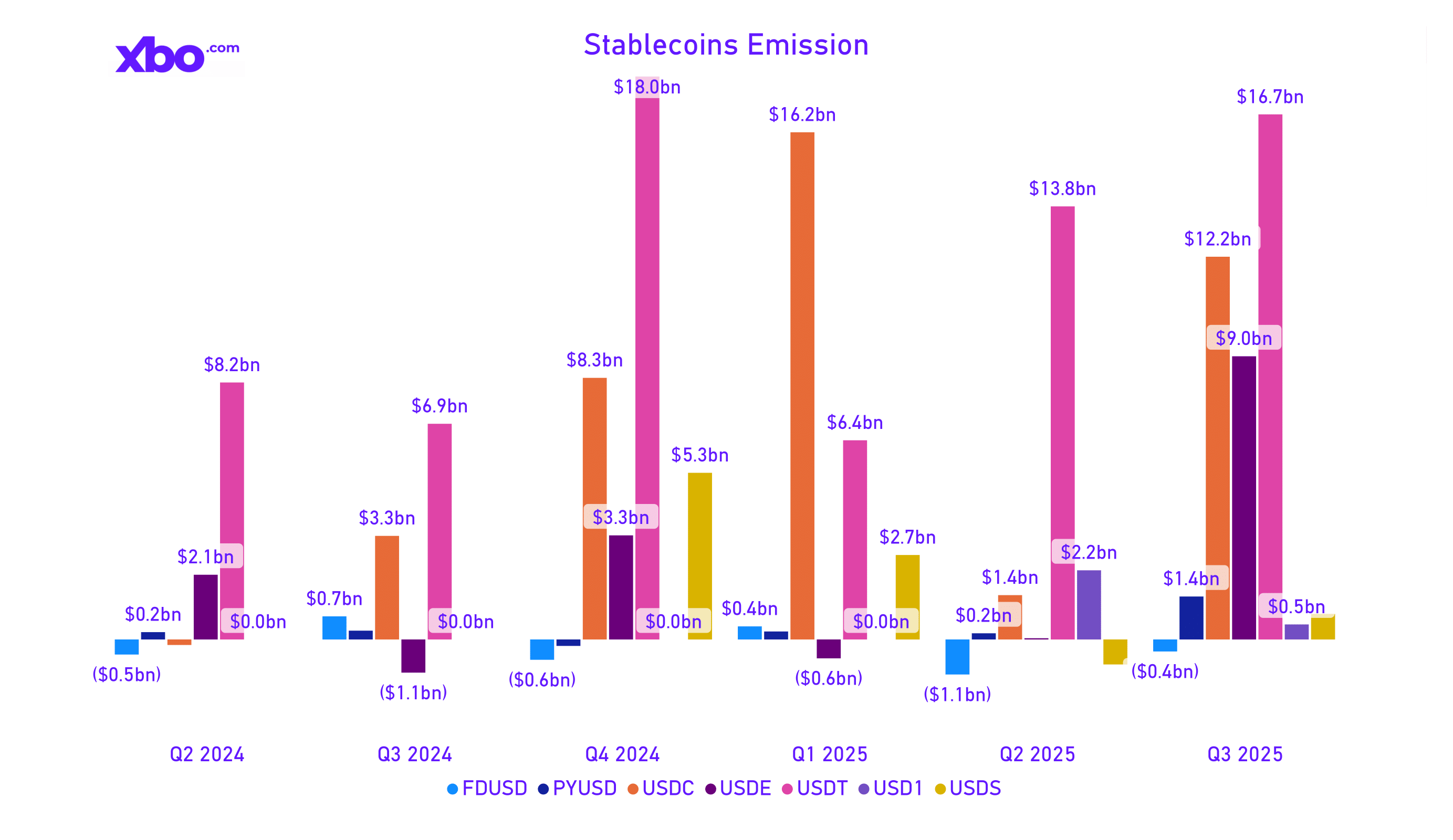

The supply of stablecoins increased by $45.3 billion over the quarter, from $244 billion to $289 billion, with a projected supply of $500 billion or more by 2026.

Source: glassnode.com

Tether and Circle remain the largest stablecoin operators, with issuance of $16.7 billion and $12.2 billion respectively. Additionally, stablecoin issuance from Ethena rose significantly, reaching $9 billion in the third quarter compared to $39 million in the second quarter.

Opportunities for International Banks

The law provides new opportunities for international banks with U.S. branches, including issuing stablecoins through an OCC license with 1:1 reserves, custody and asset storage using blockchain technology for internal operations, and cross-border transactions via reciprocal agreements with the Fed and Treasury. This strengthens protection for stablecoin holders in bankruptcy and ensures compliance with AML and BSA controls.

Actions by International Banks

HSBC submitted an OCC license application in August 2025, exploring cross-border payments. Standard Chartered is launching a pilot, investing $50 million in reserves. Deutsche Bank is collaborating with Circle for custody, testing EU-US operations. BNP Paribas has applied for a license and is developing stablecoin lending backed by $100 million in Treasuries.

Impact on the Economy and Crypto Projects

The GENIUS Act could potentially strengthen the U.S. economy. The growth of cross-border payments is estimated to add $50 billion annually to emerging markets, while demand for Treasuries will support low rates, reducing the cost of servicing public debt. For crypto projects, the law simplifies compliance and accelerates adoption, especially for issuers and bridges like LayerZero. The market capitalization of networks integrating stablecoins will likely grow due to TVL, but algorithmic stablecoins such as DAI and USDD may lose 5–10% of their share under the moratorium.

Source: app.artemisanalytics.com

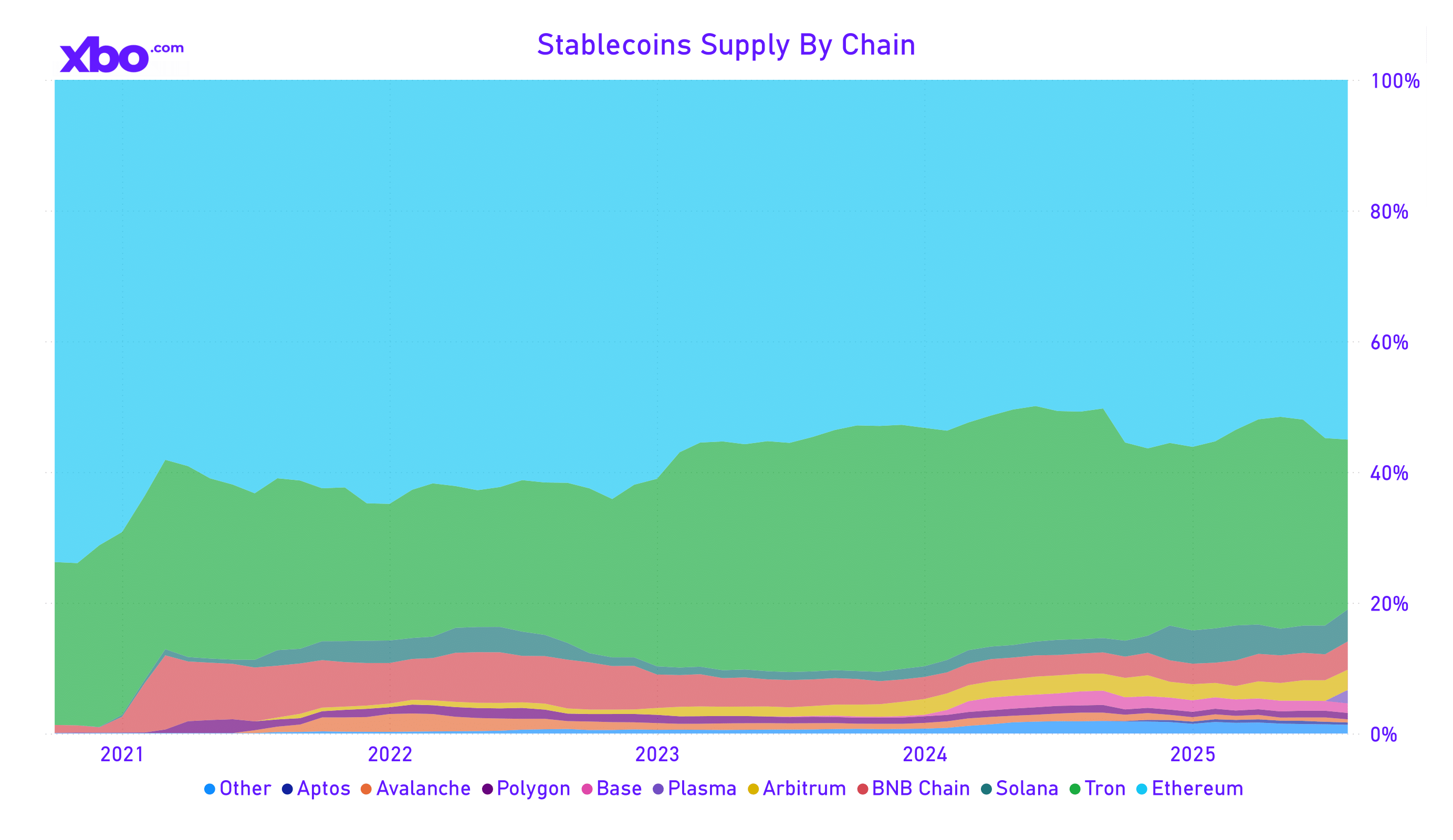

Ethereum remains the most popular blockchain for stablecoins due to its network reputation, stability, and ease of integration. Tron ranks second, driven by low transaction costs. Solana follows, with experts believing it has a strong chance to overtake the leaders in stablecoin volume as the network offers more flexible solutions for developers and benefits from existing DeFi projects on the blockchain.

Considering the above, analysts make the following forecasts:

- Lending: Aave and Compound will see a 15–25% increase thanks to bank loans, with an estimated $50 billion in liquidity.

- RWA: Asset tokenization, such as through Centrifuge, will grow by 30%, adding $10 billion by 2026.

- Cross-chain Bridges: GMP activity will increase by 20% due to bank operations.

- DEX and CEX: Trading volumes will rise by 10–15% due to increased free stablecoin liquidity.

“Quiet” Altseason

In the third quarter of 2025, the altcoin market underwent a transitional period, with a total capitalization increase of 29% and the dominance of niche themes that attracted institutional and retail capital. This was driven by a decline in BTC dominance to 57% and regulatory catalysts such as the GENIUS Act and updated generic listing standards for ETFs.

Source: app.artemisanalytics.com

Virtually all sectors showed a weighted average growth over the third quarter, aside from trending sectors like Oracle, Perp DEX, and RWA. The NFT application sector turned out to be the most profitable. Given the growth across nearly all sectors and the fact that altcoins along with ETH significantly outperformed Bitcoin while its dominance declined, a number of analysts have already dubbed the third quarter a “quiet altseason,” and based on key indicators, this is indeed the case even without the approval of spot ETFs for altcoins.

Source: defillama.com

Thanks to new regulatory opportunities, the TVL of all sectors increased by more than $44 billion over three months. It’s noteworthy that due to the RWA narrative, the capitalization and TVL of other sectors directly or indirectly related to RWA – such as Oracles, Bridges, and Lending – are growing more strongly.

Source: defillama.com

The top protocols with the highest TVL have shifted somewhat, with Morpho and Pendle displacing Uniswap and Sky. However, AAVE remains the leader, nearly doubling its TVL over the third quarter. This growth was also fueled by a focus on the RWA sector – Aave Labs introduced Horizon, an institutional platform for borrowing stablecoins like USDC from Circle, RLUSD from Ripple, and GHO from Aave, using tokenized real-world assets, such as U.S. Treasuries and BlackRock BUIDL, as collateral. This allows banks and funds to use RWA as collateral for their operations. The team also secured several partnerships focused on utilizing stablecoins and borrowing.

The Perp DEX sector deserves special attention, becoming one of the hottest narratives in altcoins by the end of the third quarter. Ethereum’s upgrade and Solana’s development have reduced transaction processing times and lowered fees, making perpetual DEXs real competitors to CEXs. At the same time, integrations with blockchains and bridges address liquidity fragmentation issues, eliminating the last hurdles for traders seeking KYC-free trading access.

Source: app.artemisanalytics.com

This has sharply increased trading volumes on perpetual DEXs, siphoning trading volumes from CEXs. On monitored exchanges alone, trading volumes reached $130 billion per day. The monthly trading volume hit $960 billion, largely thanks to Aster and the hype surrounding it.

Moreover, expectations around spot ETFs for altcoins have also become one of the key narratives, spurred by regulatory changes from the SEC. According to Bloomberg ETF analysts, the probability of ETFs for a range of altcoins being approved by year-end has reached 95–100%, which could attract $10–20 billion in institutional inflows. These expectations are based on simplified approval procedures and growing altcoin liquidity. The market anticipates approvals for major altcoins: SOL, XRP, LTC, ADA, DOGE, and AVAX. Bloomberg analysts note that the first ETFs could be approved as early as October this year, though a U.S. government shutdown might delay the process.

XBO Token

![]()

Source: www.xbo.com

Trading of the native token of XBO.com began on August 18, 2025, with a gain of over 6% in the third quarter. Despite market volatility driven by U.S. trade tariffs and economic data, the token exhibited stable price dynamics, not falling below its listing level. Toward the end of the third quarter and the start of the fourth, there has been a steady increase in trading volumes, and in early October, the token hit a new all-time high, reaching a peak valuation of $0.16042.

Source: www.xbo.com

Throughout the quarter, the ratio between sellers and buyers reflected predominantly buying activity, with an average buyer share of 56%. Price support came not only from holders but also from a recent burn of 62,500,000 XBO tokens conducted by the platform. The current circulating supply stands at 18,750,000 tokens, equivalent to 1.5% of the maximum supply. The average daily trading volumes on the XBO.com platform accounted for approximately 55% of the token’s current market capitalization, indicating significant investment and trading interest. This metric underscores active participation from both retail and institutional players, especially amid rising liquidity at the start of the fourth quarter.

The sustained growth of XBO, supported by token burns and predominant buying activity, points to a strong foundation and potential for further development. With the token reaching a new ATH and trading volumes increasing at the beginning of Q4, it is evident that market participants see its potential and are confident in its future.

Disclaimer: This article is for informational purposes only and not financial advice. XBO makes no guarantees about the data's accuracy. Readers should consult an advisor before making decisions and are responsible for their actions.